Many entrepreneurs start businesses because they are good at building products, solving problems, or serving customers — not to deal with accounting.

Yet every business eventually reaches a point where financial clarity becomes unavoidable. Revenue grows, expenses increase, taxes arise, and decisions begin to rely more on numbers than intuition.

This is where financial reporting for entrepreneurs becomes important. Not in the traditional accounting sense filled with technical terminology, but in a practical sense that helps business owners understand what is actually happening inside their company.

Financial reporting does not have to be complex. When simplified correctly, it becomes one of the most useful tools an entrepreneur can have.

Why Financial Reporting Feels Difficult for Entrepreneurs

Many small business owners feel intimidated by financial reporting for a simple reason: most accounting systems are built for accountants.

Traditional reporting structures often assume knowledge of terms such as accruals, depreciation schedules, cost allocations, or tax adjustments. For someone running a small business, these concepts can feel disconnected from daily operations.

Research published by the International Federation of Accountants (IFAC) notes that many small and medium enterprises struggle with financial reporting because systems are designed around professional accounting workflows rather than the needs of owner-operators.

Entrepreneurs usually want answers to much simpler questions. They want to know whether the business is profitable, where money is going, and which activities generate the most value. Financial reporting should provide clarity around those questions rather than introduce additional complexity.

The Three Financial Reports Every Entrepreneur Should Understand

Entrepreneurs do not need to master every accounting document. In practice, most business decisions depend on only a few core financial reports.

Profit and Loss Statement

The profit and loss report, often called the P&L, shows how much money the business earned and how much it spent during a specific period.

This report summarizes revenue, operational costs, and the final profit or loss for the business. It is the fastest way to understand whether a company is financially sustainable.

According to guidance from the U.S. Small Business Administration (SBA), the profit and loss statement is the most widely used financial report among small businesses because it provides a clear picture of operational performance.

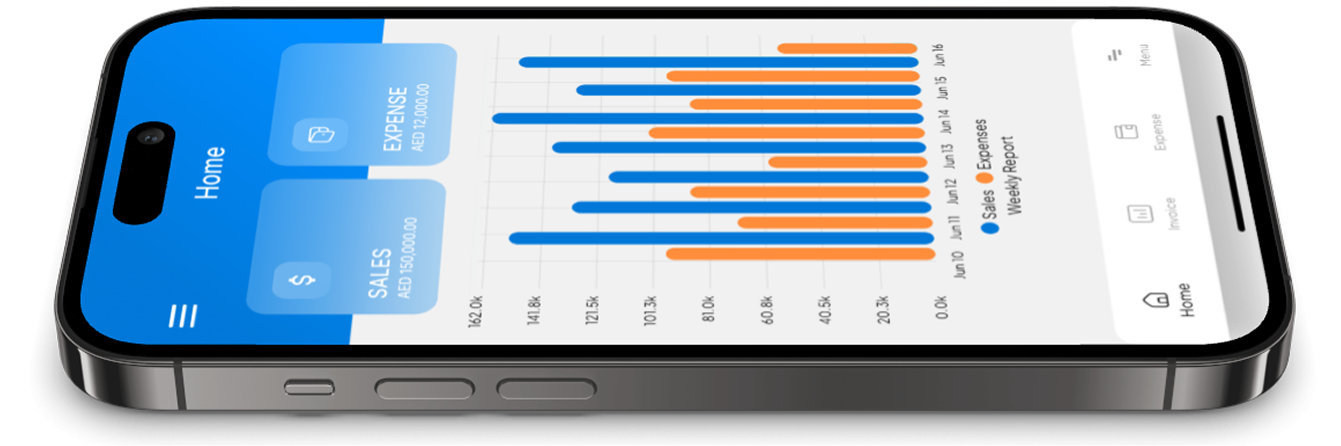

Many modern tools simplify this process by generating a P&L automatically as transactions are recorded. Platforms such as BookBI, for example, present profit and expense information through a simple dashboard rather than traditional accounting tables, making it easier for entrepreneurs to see their financial position without needing accounting expertise.

Cash Flow Overview

Profit alone does not always reflect the real financial health of a business. A company may technically be profitable while still struggling to pay bills if cash arrives too slowly.

Cash flow reporting focuses on how money moves through the business over time. It shows when funds enter the company and when payments leave.

The Harvard Business Review has repeatedly emphasized that poor cash flow management is one of the most common reasons small businesses encounter financial difficulties. Entrepreneurs often underestimate how quickly liquidity problems can appear when invoices remain unpaid or expenses grow unexpectedly.

Clear visibility into invoices and payments helps reduce this risk. Tools designed for small businesses increasingly include automated invoicing and payment tracking. For instance, systems like BookBI allow entrepreneurs to generate VAT-compliant invoices quickly and monitor receivables in real time, which helps maintain a healthier cash flow without constant manual follow-up.

Balance Overview

The balance sheet shows the overall financial position of a business at a specific moment. It summarizes assets, liabilities, and owner equity.

For early-stage entrepreneurs, this report may feel less urgent than profit or cash flow reporting. However, it becomes increasingly important as businesses grow and begin working with investors, lenders, or partners.

The balance sheet helps external stakeholders evaluate the stability and financial structure of the company. Even when entrepreneurs rely on an accountant for formal reporting, having a simplified overview of assets and obligations can help them understand the broader financial picture of their business.

Why Real-Time Financial Visibility Matters

Historically, financial reports were produced monthly or quarterly by accountants. In modern business environments, this delay can limit the usefulness of financial data.

Entrepreneurs often need to make decisions quickly. Marketing costs may increase unexpectedly, suppliers may adjust pricing, or new opportunities may appear that require immediate investment.

Industry analysts from Deloitte’s small business finance research highlight that real-time financial visibility allows entrepreneurs to react faster to changes in their business environment. When revenue and expenses update continuously, owners gain a clearer understanding of how their company evolves over time.

Instead of waiting weeks for financial summaries, entrepreneurs can monitor performance while decisions are still relevant.

Some financial tools are increasingly designed with this in mind. Rather than producing reports only at the end of a month, platforms like BookBI maintain continuously updated dashboards where revenue, expenses, and net position are visible at any time. This kind of real-time overview can help entrepreneurs stay closer to the financial pulse of their business.

Common Financial Reporting Mistakes Entrepreneurs Make

Entrepreneurs who manage finances without formal accounting experience often encounter a few predictable challenges.

- Relying heavily on spreadsheets

While spreadsheets offer flexibility, they become difficult to manage as transaction volumes grow. Manual data entry also increases the risk of small errors that can accumulate over time. - Infrequent financial review

Many entrepreneurs review financial reports only occasionally — often once a month when their accountant prepares statements. By then, the information may already be outdated and less useful for decision-making. - Disorganized documentation

Lost receipts, scattered invoices, and incomplete records make it difficult to maintain accurate financial data. This can also create complications during audits or tax filings.

Digital document management has become increasingly helpful here. Some accounting platforms allow receipts to be photographed and automatically stored alongside transactions. In tools like BookBI, receipts can be scanned directly through the mobile interface and archived digitally, helping entrepreneurs avoid the common problem of misplaced paperwork.

Making Financial Reporting Simpler

Technology has significantly changed how small businesses handle financial reporting. Modern accounting tools increasingly focus on automation and usability rather than technical accounting terminology.

Instead of manually entering every transaction, many systems now capture financial data automatically. Receipts can be scanned with mobile devices, expenses categorized automatically, and invoices generated instantly.

Digital dashboards allow entrepreneurs to view revenue, expenses, and profit in real time. This removes much of the administrative work that once made financial reporting feel overwhelming.

According to a PwC report on digital finance tools, automation can reduce administrative accounting work in small businesses by up to forty percent. This shift allows entrepreneurs to spend less time on bookkeeping and more time focusing on strategy and growth.

Some platforms designed specifically for entrepreneurs, including BookBI, take this approach further by minimizing accounting jargon altogether. Instead of complex menus or technical reports, they focus on simple actions such as recording expenses, issuing invoices, and viewing profit trends.

Financial Reporting as a Decision Tool

When financial reporting becomes clear and accessible, it evolves into more than a compliance requirement. It becomes a strategic tool.

Entrepreneurs who regularly review financial data gain insights that influence everyday decisions. They can identify which products generate the highest margins, which clients produce the most reliable revenue, and which expenses no longer justify their cost.

Instead of relying on intuition alone, decisions can be supported by measurable financial information.

Over time this clarity improves the overall stability of the business. Problems become visible earlier, opportunities become easier to evaluate, and growth decisions become more informed.

For many entrepreneurs, tools that simplify financial reporting — solutions like BookBI — make this process easier by turning complex financial data into simple visual insights that can be understood quickly.

A Simpler Future for Entrepreneurial Finance

The financial technology industry increasingly recognizes that entrepreneurs need different tools than professional accountants.

New platforms emphasize clarity, automation, and usability. Rather than overwhelming users with dozens of technical reports, they focus on presenting the financial information entrepreneurs actually need to run their businesses.

Professional accountants still play an important role in areas such as tax planning and compliance. However, everyday financial awareness no longer requires specialized training.

With the right tools and a basic understanding of key reports, financial reporting for entrepreneurs can become straightforward, accessible, and genuinely valuable.

If you are an entrepreneur looking for a simpler way to manage finances, tools like BookBI can help automate reporting, track performance in real time, and turn complex numbers into clear business insights. The right system makes financial reporting less about accounting, and more about decision-making.